When it comes to pension funds, returns are one thing, but volatility matters, too. And chasing higher returns increases their volatility, effectively reducing those returns over time. Pension funds typically pay out more in benefits than they take in via contributions. Therefore, these reduced returns are especially costly when trying to recover from underfunding; investment returns must not only make up that difference, they must also help replenish Net Assets. Bad years hurt more than good years help.

Let’s look at how much that volatility costs, and how much it has cost Colorado’s Public Employees Retirement Association (PERA) in particular since 2000.

Averages and Volatility

Pension plans base their calculations on a constant expected return. Because returns multiply over time to create a multi-year cumulative return, even if the plan averages its target return over a number of years, it will realize a lower cumulative return.

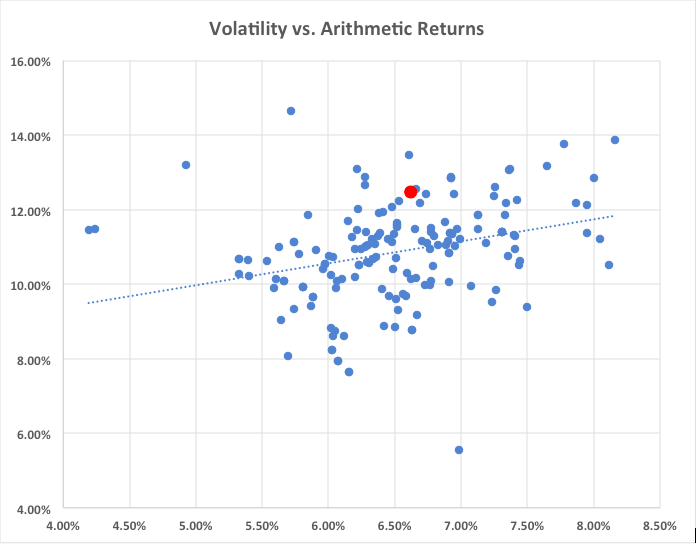

The following chart compares the arithmetic average returns and volatilities since Fiscal Year 2001 of 150 distinct public pension funds tracked by the Center for Retirement Research at Boston College. The data includes the latest fiscal year, whether 2017 or 2018.

As expected, volatility increases with returns, with considerable variation in volatility even in funds with comparable returns. The red dot is PERA; its volatility is among the highest for funds with similar returns.

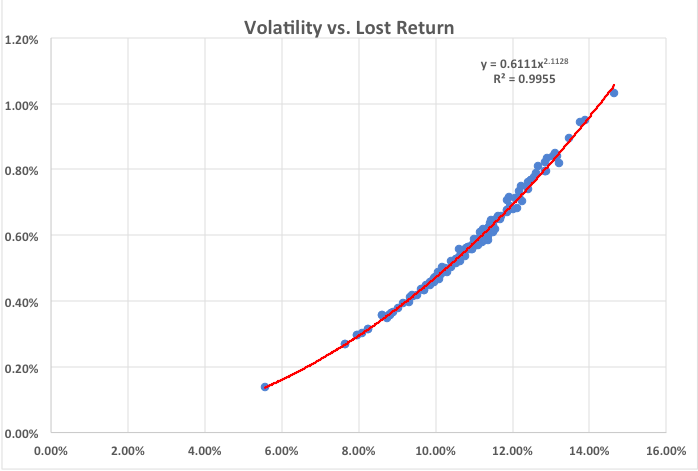

If a fund returned its arithmetic average every year, that would also be its geometric average. The difference between that and its actual geometric average we may consider to be returns lost to volatility. While there may be a closed-form solution, the data from the last 18 years can be fitted quite closely:

The volatility of PERA’s returns is 12.48%, which corresponds to an annual lost return of 0.78%. PERA’s actual lost return is 0.77% for a cumulative average return of 5.85% instead of 6.62%. Compare that to the Nevada Regular Employees Fund:

| PERA | Nevada Regular Employees | |

| Average Return (Rank of 150) | 6.62% (73) | 6.63% (70) |

| Volatility | 12.48% | 8.78% |

| Geometric Return (Rank of 150) | 5.85% (91) | 6.27% (50) |

This is not an aberration. We can similarly compare the Texas Municipal fund to the Louisiana Employee Retirement System which start out with nearly identical average returns, but diverge from volatility:

| Texas Municipal | Louisiana ERS | |

| Average Return (Rank of 150) | 6.98% (36) | 6.97% (37) |

| Volatility | 5.56% | 11.48% |

| Geometric Return (Rank of 150) | 6.84% (11) | 6.36 (39) |

PERA does report average multi-year returns as the geometric average, not the arithmetic average, which is correct. What they repeatedly fail to acknowledge is that chasing higher returns results in increased volatility, and that that volatility costs them returns. It makes it harder to achieve the average returns they need, and even when they do, it means they’re making less than they could.

What’s more, those returns need to do double duty. Because PERA is underfunded, they need to make up the annual difference between contributions and benefits and help replenish the Net Position. Since bad years hurt more than good years help, and since greater volatility increases both the frequency and severity of bad years, volatility is the enemy of long-term solvency.

Joshua Sharf is a fiscal policy analyst at the Independence Institute, a free market think tank in Denver.