Last year, just before Covid upended the world, Channel 4 reported that Denver’s Employee Retirement Program (DERP) had overpaid about $11 million in pension benefits over the course of 15 years. That became the catalyst for a look at the overall health of the pension plan.

We found that the plan had a little under $1.4 billion in unfunded liabilities, and only about 62 cents on hand for every dollar of expected liabilities, meaning it was funded at about 62%. The actual rates of return on investment were volatile; bad years took a greater toll on the plan’s funding than good years could make up. Because contributions had to keep increasing just to keep pace with benefits paid, less than 40% of benefits were being paid out of investment earnings, down from 55% a decade earlier.

Eighteen months later and DERP still has problems. It is also evident that the plan would be better off with a passive investment strategy.

Despite a 12.6% return in 2019, and a 5.7% return in 2020, the funded level has dropped to just over 60%, and the unfunded liability has risen to over $1.5 billion (see graph 1).

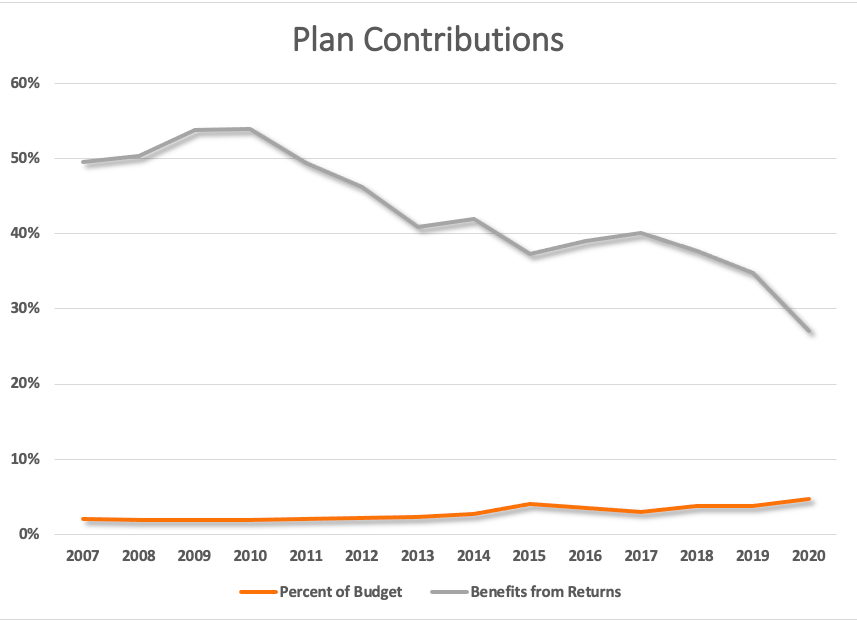

This has happened even as benefits have leveled off and contributions have increased. Contributions now comprise nearly 75% of benefits, with only 27% of benefits being paid for from investment returns. Worse, they are beginning to be a serious factor in city finances. In 2020, just the pension portion of the contribution from the City & County of Denver came to 4.7% of the total budget for government and business-type activities (see graph 2).

This is where a new analysis of large pension funds nationally produces results that are both hopeful and instructive.

Richard Ennis, one of the pioneers of quantitative investing and former executive editor of the CFA Institute’s Financial Analysts Journal, has issued a new paper showing that 1) most pension funds choose benchmarks that are designed to make their returns look good, and 2) could achieve equivalent or better results by passive investment in a few representative index funds.

Using a technique developed by Stanford’s William Sharpe, who helped originate the Capital Asset Pricing Model, Ennis created a portfolio of three indexes, and find the mix whose returns mostly closely matched a given fund’s returns from 2010-2020. In effect, we are finding the amount of risk the fund is willing to assume, and that created “portfolio” shows the overall market return for a given risk. By comparing the returns from this portfolio to the fund’s actual returns, we can see if the fund is outperforming the market.

I performed the same analysis for DERP from the years 2007-2020, using the same three indexes. Those indexes represent US stocks, US bonds, and international stocks. That portfolio, consisting of roughly 33% US stocks, 45% US bonds, and 22% foreign stocks, would have returned an average of 6.5% per year over that period, compared to the 5.6% the fund actually returned. It would also have achieved those returns will slightly less volatility, a standard deviation in returns of 10.7% vs. the fund’s actual 11.2%.

Understand that these three indexes are all tracked by investable funds. This means that it would be easy for a pension fund to buy those funds in whatever proportion it wanted, and let the fund managers do the work, rather than paying investment analysts of its own. Had the fund done that, we estimate that it would have $250 million more in assets from saved investment fees plus the investment returns on those fees. We also estimate that there might have been as much as an additional $500 million in assets based just on the improved returns. That would be enough to cut the unfunded liability in half.

The one caveat here is that we don’t really know what the funding policy decisions would have been if the fund hadn’t been so underfunded along the way. It’s possible that, with better funding levels, the city’s contribution levels wouldn’t have risen the way they have.

Nevertheless, given the increasing pressure on the city budget, perhaps it’s time for the city government to ask what value the pension’s fund managers are adding, and whether or not they’re costing more than they’re helping.

Joshua Sharf is a senior fellow in fiscal policy at the Independence Institute, a free market think tank in Denver.